Timelines

Jun - Nov 2025

Role

Lead UX/UI Designer

Team

1 Designer

1 Product Manager

6 Engineers

Skills

User research

User flows

Product Design

Usability testing

Overview

Select by Urban Jungle is a non-standard home insurance product built in partnership with Prestige Underwriting. It’s purpose is to cover people with unique homes or circumstances who were previously uninsurable through Urban Jungle’s standard home journey.

I led the product design work stream for the full launch, from initial research through to high-fidelity delivery of a new design system, the direct purchase journey, account manager and marketing flows. The goal was to make a historically complex insurance experience feel simple and human.

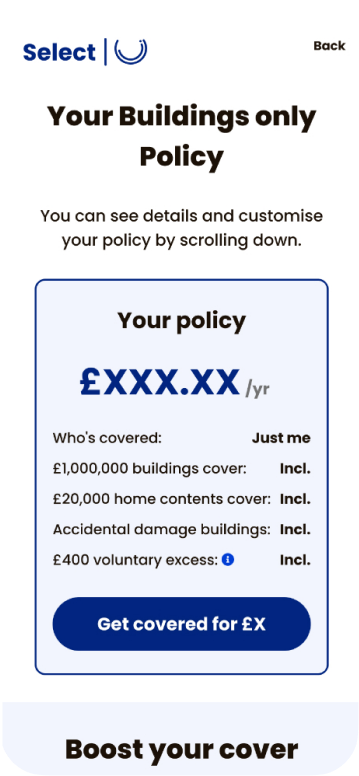

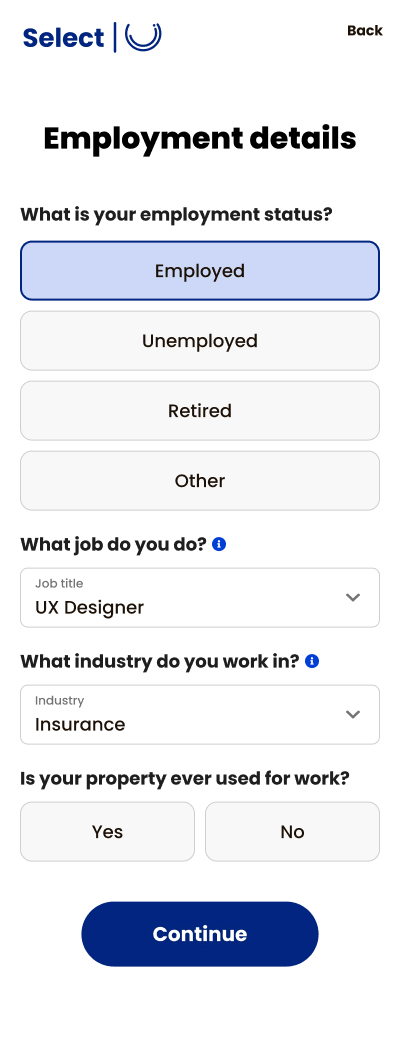

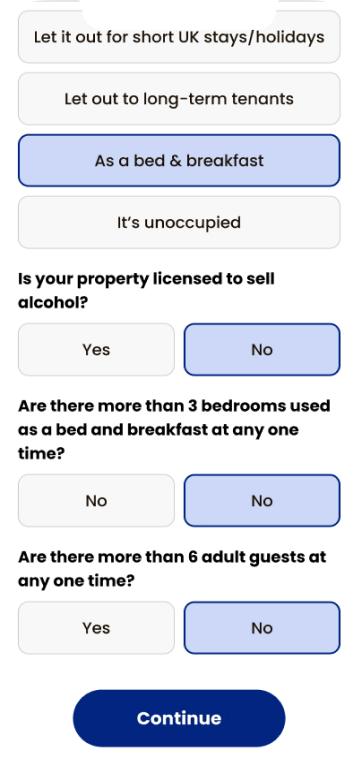

Creating different flows for different needs

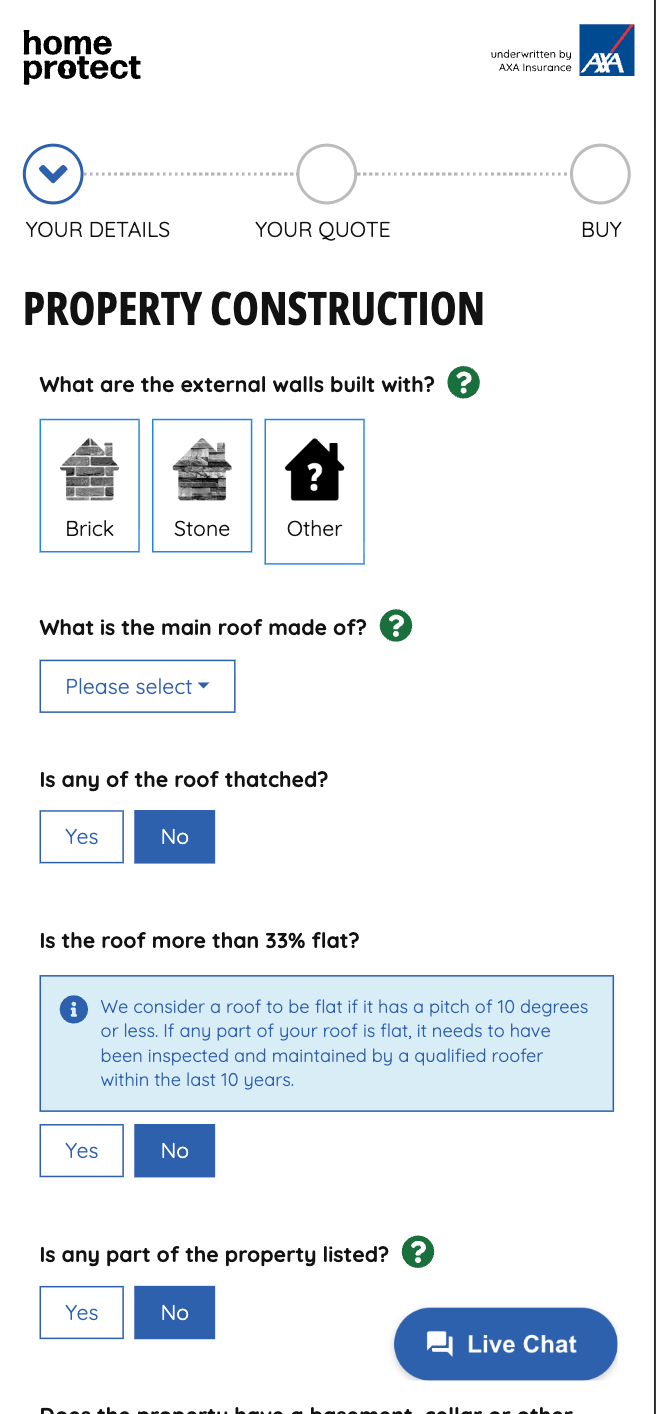

A month before launch, underwriters mandated expanding our Building and Contents MVP to the full product. The goal was to accommodate complex edge cases across multiple user profiles without building separate, siloed journeys.

We tailored the dynamic flow based on the customer's specific property profile:

Buildings only

We removed irrelevant contents questions and cover options to streamline the journey.

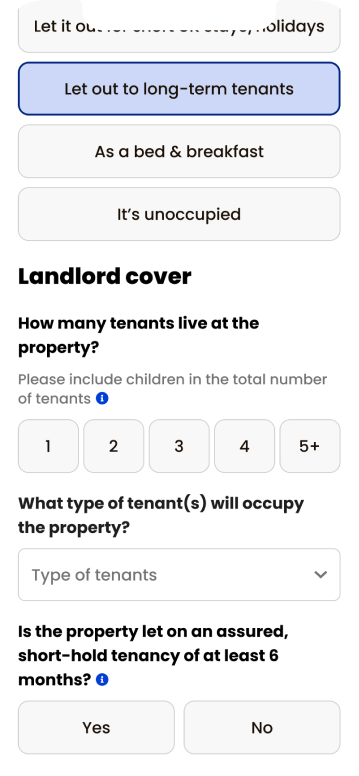

Landlords

We added targeted property questions and integrated landlord-specific add-ons.

Unoccupied

We restructured our package to offer specific, tiered levels of cover for empty properties.

Select by Urban Jungle | Shipped Nov 2025

Urban Jungle's entry into the non-standard home insurance market

Problem

We turn away 1 in 4 customers and they don’t know why.

Urban Jungle currently can't quote for 26% of customers who start a home insurance quote. This is because underwriters don’t like to cover customers with unusual properties or unique personal circumstances.

It requires more information

Covering them requires a much longer, jargon-heavy journey because their risk is more complex, so insurers needs more information to cover them which the industry has never solved well. The result is almost always the same: fill out a long form and be forced to call up anyways.

You can be non-standard without knowing it

A lot of customers don't know they're non-standard. Someone with a larger home or an unknown County Court Judgment doesn't expect to be turned away — they just feel rejected by Urban Jungle, with no explanation and no path forward.

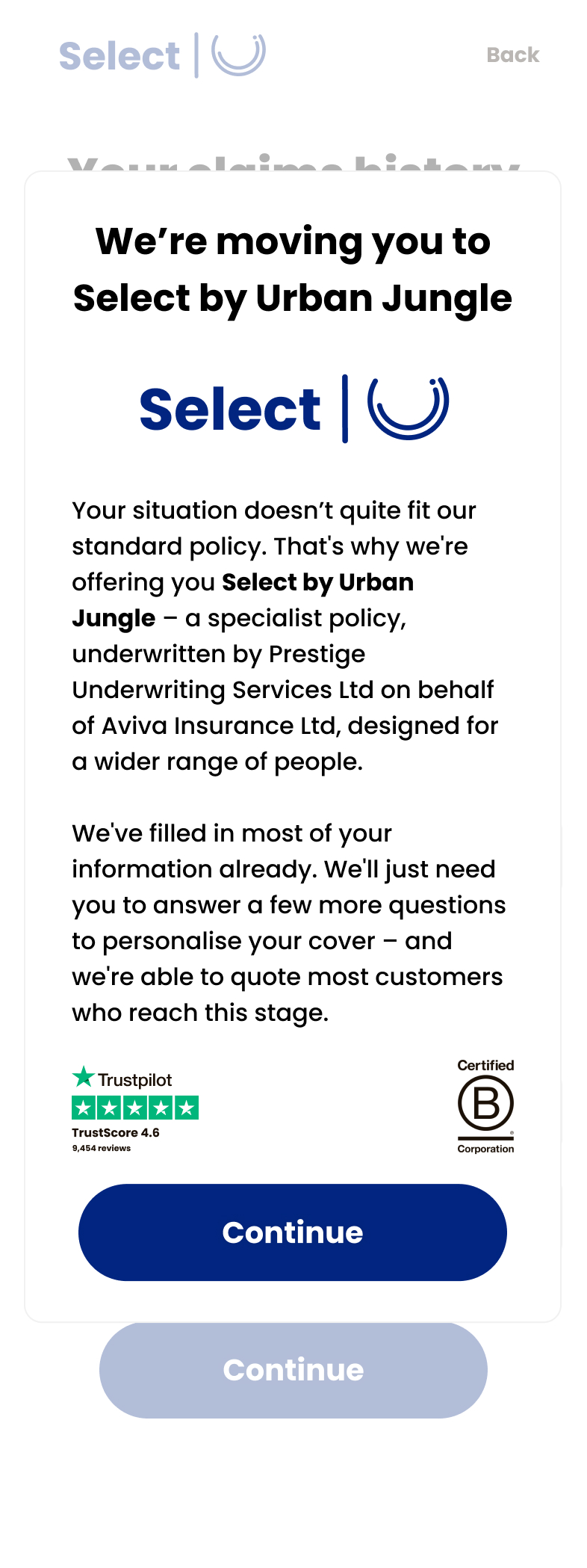

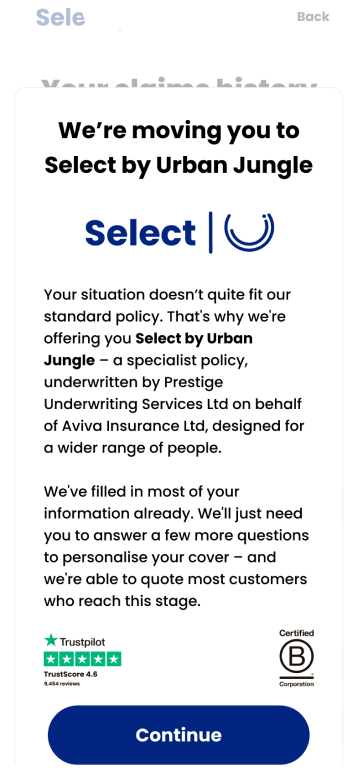

Branding

Select needed its own brand

Our standard product claims (from £5/month, rolling plans, age-blind pricing) didn't apply here. Using them would mislead customers.

The fix: a distinct sub-brand with its own name, logo, and colour — dark blue #012580 — that clearly signals a different, tailored product while staying within the Urban Jungle family.

Brand guide

Typography

Aa

Poppins

Medium, SemiBold, Bold, ExtraBold, Black

Heading 1

Heading 2

Body

Microcopy

ExtraBold

Bold

Medium

SemiBold

30pt

18pt

18pt

14pt

How to move customers into our journey

Most users don't know they're non-standard. Instead of telling them they've "failed," we used a modal transition. This kept them in the UJ environment, explaining the tailored journey ahead, and auto-filling all previously entered data.

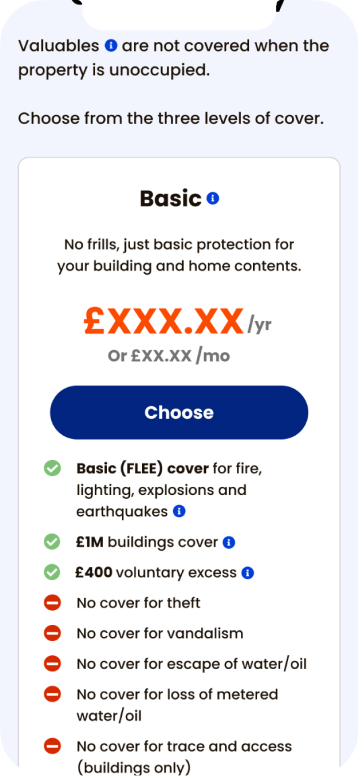

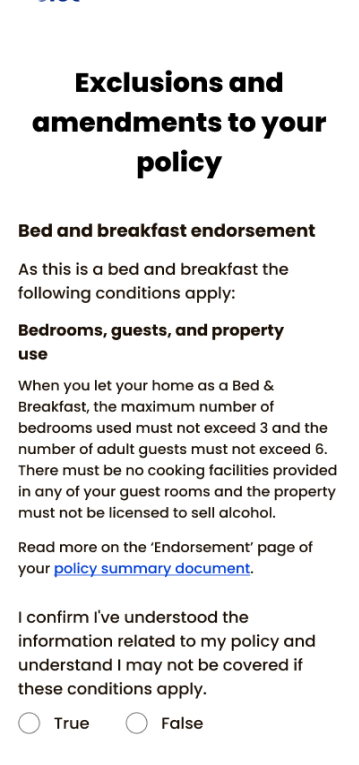

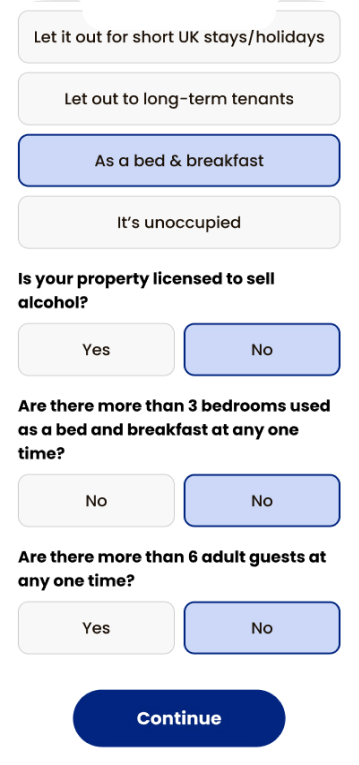

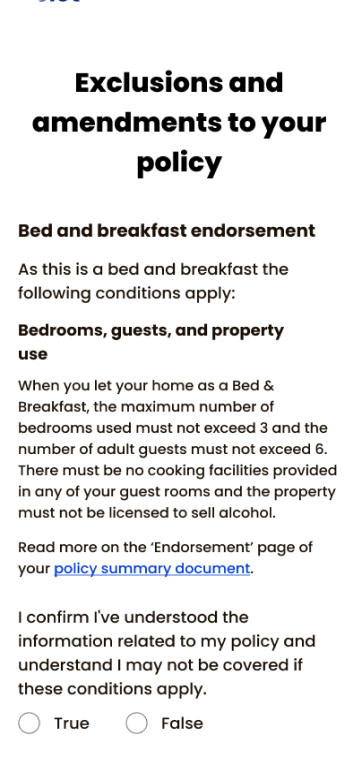

Handling endorsements

Endorsements are written changes to an insurance policy that add, change, or remove cover based on a customer's circumstances. The goal was to be better than the industry standard by being transparent so customers are aware of any policy limitations before they purchase.

We tailored how we surface this information based on how much it could affect a customer:

Additional questions

If a condition would void all cover, we added direct questions upfront to avoid offering a policy that was unfair to customers.

Warning messages or an exclusions page

Important conditions are flagged via warning messages or a dedicated page the customer must confirm they've read.

Outcome

What was delivered

A specialist sub-brand that feels like a recommendation, not a rejection.

Select by Urban Jungle launched as an MVP covering complex risks: unoccupied properties, holiday homes, landlord cover, listed buildings, renovation works, and adverse financial history.

MARKET REACH

88%

of UK homes can now get cover, including properties our standard insurance decline

CONVERSION LIFT

3%

increase in overall conversion across Urban Jungle, driven by Select

ELIGIBILITY UPLIFT

26%

more customers are now eligible for Urban Jungle home insurance, due to Select's extended cover

DROP OFF RATE

2.5%

3 x lower than the 9.5% drop-off when customers were referred to Paymentshield, a partner insurer

Research

Mapping the market

I analysed numerous non-standard insurers to understand their flows, question sets, and drop-off points. This surfaced friction patterns that make or break a complex purchase journey.

Design

Our problems and deliberate decisions

Turning our research into a functional UI meant tackling a few major hurdles. The goal was to move away from the industry norm of endless forms and toward a journey that felt tailored and transparent.

Reflection

What I learnt

Rejection is a UX problem and the way it’s framed matters enormously. Moving a customer to a specialist product can feel like personalisation or like failure. The design decides which.

Transparency reduces friction downstream. Pulling endorsement fine print into the UI cuts support tickets and builds genuine trust. Customers who understand what they're buying don't need to call.

Reflection

What I learnt

Rejection is a UX problem and the way it’s framed matters enormously. Moving a customer to a specialist product can feel like personalisation or like failure. The design decides which.

Transparency reduces friction downstream. Pulling endorsement fine print into the UI cuts support tickets and builds genuine trust. Customers who understand what they're buying don't need to call.

Select by Urban Jungle | Shipped Nov 2025

Urban Jungle's entry into the non-standard home insurance market

Timelines

Jun - Nov 2025

Role

Lead UX/UI Designer

Team

1 Designer

1 Product Manager

6 Engineers

Skills

User research

User flows

Product Design

Usability testing

Overview

Select by Urban Jungle is a non-standard home insurance product built in partnership with Prestige Underwriting. It’s purpose is to cover people with unique homes or circumstances who were previously uninsurable through Urban Jungle’s standard home journey.

I led the product design work stream for the full launch, from initial research through to high-fidelity delivery of a new design system, the direct purchase journey, account manager and marketing flows. The goal was to make a historically complex insurance experience feel simple and human.

Problem

We turn away 1 in 4 customers and they don’t know why.

Urban Jungle currently can't quote for 26% of customers who start a home insurance quote. This is because underwriters don’t like to cover customers with unusual properties or unique personal circumstances.

It requires more information

Covering them requires a much longer, jargon-heavy journey because their risk is more complex, so insurers needs more information to cover them which the industry has never solved well. The result is almost always the same: fill out a long form and be forced to call up anyways.

You can be non-standard without knowing it

A lot of customers don't know they're non-standard. Someone with a larger home or an unknown County Court Judgment doesn't expect to be turned away — they just feel rejected by Urban Jungle, with no explanation and no path forward.

Research

Mapping the market

I analysed numerous non-standard insurers to understand their flows, question sets, and drop-off points. This surfaced friction patterns that make or break a complex purchase journey.

Branding

Select needed its own brand

Our standard product claims (from £5/month, rolling plans, age-blind pricing) didn't apply here. Using them would mislead customers.

The fix: a distinct sub-brand with its own name, logo, and colour that clearly signals a different, tailored product while staying within the Urban Jungle family.

Brand guide

Typography

Aa

Poppins

Medium, SemiBold, Bold, ExtraBold, Black

Heading 1

Heading 2

Body

Microcopy

ExtraBold

Bold

Medium

SemiBold

30pt

18pt

18pt

14pt

How to move customers into our journey

Most users don't know they're non-standard. Instead of telling them they've "failed," we used a modal transition. This kept them in the UJ environment, explaining the tailored journey ahead, and auto-filling all previously entered data.

Creating different flows for different needs

A month before launch, underwriters mandated expanding our Building and Contents MVP to the full product. The goal was to accommodate complex edge cases across multiple user profiles without building separate, siloed journeys.

We tailored the dynamic flow based on the customer's specific property profile:

Buildings only

We removed irrelevant contents questions and cover options to streamline the journey.

Landlords

We added targeted property questions and integrated landlord-specific add-ons.

Unoccupied

We restructured our package to offer specific, tiered levels of cover for empty properties.

Handling endorsements

Endorsements are written changes to an insurance policy that add, change, or remove cover based on a customer's circumstances. The goal was to be better than the industry standard by being transparent so customers are aware of any policy limitations before they purchase.

We tailored how we surface this information based on how much it could affect a customer:

Additional questions

If a condition would void all cover, we added direct questions upfront to avoid offering a policy that was unfair to customers.

Warning messages or an exclusions page

Important conditions are flagged via warning messages or a dedicated page the customer must confirm they've read.

Outcome

What was delivered

A specialist sub-brand that feels like a recommendation, not a rejection.

Select by Urban Jungle launched as an full product covering complex risks: unoccupied properties, holiday homes, landlord cover, listed buildings, renovation works, and adverse financial history.

MARKET REACH

88%

of UK homes can now get cover, including properties our standard insurance decline

CONVERSION LIFT

3%

increase in overall conversion across Urban Jungle, driven by Select

ELIGIBILITY UPLIFT

26%

more customers are now eligible for Urban Jungle home insurance, due to Select's extended cover

DROP OFF RATE

2.5%

3 x lower than the 9.5% drop-off when customers were referred to Paymentshield, a partner insurer

Design

Our problems and deliberate decisions

Turning our research into a functional UI meant tackling a few major hurdles. The goal was to move away from the industry norm of endless forms and toward a journey that felt tailored and transparent.

Reflection

What I learnt

Rejection is a UX problem and the way it’s framed matters enormously. Moving a customer to a specialist product can feel like personalisation or like failure. The design decides which.

Transparency reduces friction downstream. Pulling endorsement fine print into the UI cuts support tickets and builds genuine trust. Customers who understand what they're buying don't need to call.